Describing the alternatives for decarbonizing the economy

Neus Casajuana

In article 1 we gave an overview of how the issue of decarbonization of the European economy has been addressed so far. We summarized the different measures being implemented to achieve behavioral changes in citizens and companies towards attitudes more consistent with the goal of achieving climate neutrality by 2050. We gave a brief description of the two main mechanisms being used to achieve these changes: carbon taxes and the emissions market. We also presented two alternative theoretical proposals to these mechanisms, based on the establishment of a cap, a concrete limit to the emissions of the real economy that include both the sectors subject to the emissions market and the rest of the emissions (approx. 55% of the total) coming from the rest of the activities of citizens and companies not subject to the emissions market. These decarbonization pathways have not been implemented so far, probably due to their radical nature: «Cap and Dividend» and «Tradable Energy Quotas» (TEQs). In this article we will develop these two proposals in more detail, showing their similarities and differences. We will also present a modification of TEQs that from now on we will call EcoCore.

What do the two proposals «Cap and Dividend» and «Tradable Energy Quotas» have in common?

Both proposals are based on setting an annual cap on greenhouse gas emissions, consistent with the EU carbon budget and with the objective of reaching climate neutrality by 2050. To this end, an annual and gradual reduction of this emissions cap is established in order to meet the commitments we have set ourselves: a 55% reduction in emissions by 2030 (Fit 55) and zero carbon by 2050.

The two proposals make all citizens and companies co-responsible for reducing their emissions in the fairest way possible. Both proposals redistribute equally the co-responsibility for reducing emissions.

The way to redistribute emissions is based on the issuance, by a Public Agency, of a certain number of greenhouse gas emission Permits or carbon rate Energy Quotas (each unit of a carbon rate Energy Quota is equivalent to a quantity of CO2 ). The aggregate of the units of Energy Quotas or emission permits will be equal to the emissions cap imposed for that year.

Here is an example:

Ex: 1 Emission Permit = (equivalent to generate ) 1 kg. of CO2.

Ex: 1 Unit of Energy Quota = an amount of Energy equivalent to 1 kg. of CO2.

The reduction of emissions reaches all sectors of the economy. This differentiates both proposals from the current emission allowance market that only applies to some sectors that are responsible for less than half of the emissions emitted in the whole economy.

The optimal way to implement both proposals would be to integrate all countries in the world. But until a global agreement is reached, it is possible to tailor the measures to a region (the EU) and even to an individual country, albeit with limitations.

To protect the region applying these measures from unfair competition, border restrictions would logically have to be implemented by applying climate tariffs to all imports from countries with fewer climate obligations.

How do the two proposals «Cap and Dividend» and «Tradable Energy Quotas» differ?

The basic differences between the two proposals are in the way these allowances are allocated and in the purchase value of these allowances.

Below we describe and show three operating schemes corresponding to the «Cap and Dividend», «Tradable Energy Quotas» (TEQs) traditional Mode and «Tradable Energy Quotas» Mode 2 (TEQs Mode 2) proposals.

«Cap and Dividend»

Emission permits are distributed only among fossil energy producing companies through an auction (Fig 1). All fossil energy producing companies are required to attend the auction to obtain their annual emission permits. The monetary value of the permits is determined at each auction. All money collected at the auctions is redistributed equally among all citizens.

Fig. 1 Circulation of emission permits P and money $ in the economy in «Cap and Dividend».

The detail of «Cap and Dividends» operational mechanism is described in this link: https://capglobalcarbon.org/2021/08/31/how-it-works/

«Tradable Energy Quotas» (TEQs)

TEQs

Citizens receive a quota (an amount) of carbon rate energy, which from now on we will call permits because these fossil energy quotas are equivalent to a certain number of permits depending on the carbon contained in the energy (Fig. 2). The permits are distributed among citizens free of charge by the Public Agency, but non-energy companies and the government must buy them. When companies, the government or citizens go to buy energy (electricity, gas, gasoline), in addition to paying the price of the product, we will have to deliver an amount of permits, depending on the amount of carbon incorporated in each of these energy sources. All these transactions are done automatically through a digital wallet in which we will have our permits and our money.

In addition to this initial distribution, there will be a secondary market in which citizens and companies can sell or buy the permits if they have a surplus or a deficit, depending on their needs.The permits held by companies, government and citizens will be paid as energy is purchased, together with the energy price in currency. Each fuel, depending on the amount of carbon it contains, will require more or fewer permits. Green energy would require 0 permits. At the end of the period, energy companies must hand over the permits to the Public Agency that manages the system.

Non-energy companies are expected to raise their prices to compensate for the cost of permits, and to translate it to consumer prices, at least to some extent. This is expected to create an incentive for economic transformation in search for a lower energy consumption.

Fig. 2 Circulation of emission permits P in the economy in traditional TEQs model.

The TEQs operational mechanism is described in this link: https://www.flemingpolicycentre.org.uk/teqs/

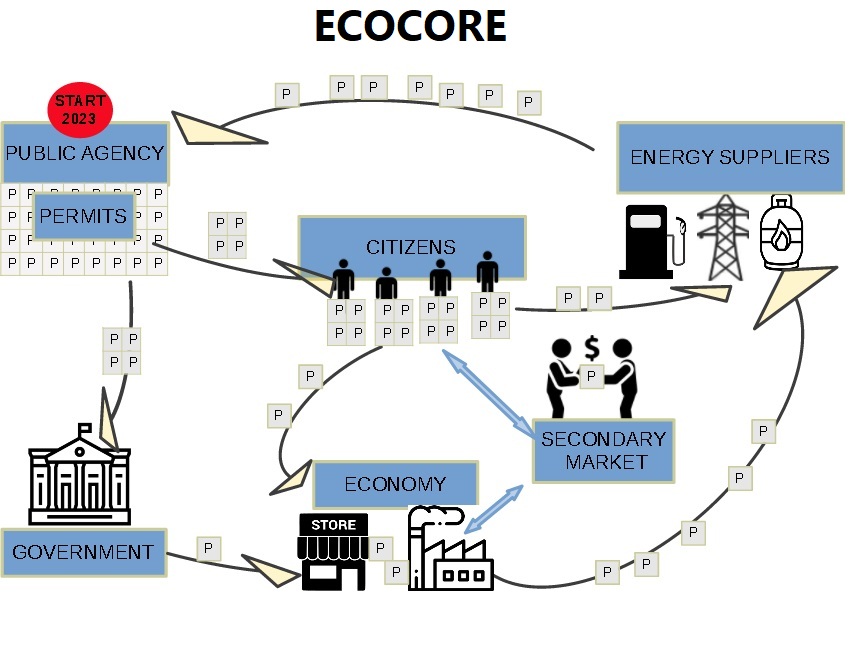

EcoCore

The difference with TEQs lies in two characteristics: 1º The permits issued in this case are directly CO2 emission permits, instead of fossil energy quotas. 2º The way in which non-energy and non-exporting companies obtain the permits: while in TEQs these companies must buy the permits from the Public Agency that manages the system, or in the secondary market, in the EcoCore Model there won’t be an initial sale of permits to these companies, although they can still buy them in the secondary market. On the other hand, citizens will get a higher amount of permits instead. This means that these companies must get the permits by charging the citizens for them, or buy them in the secondary market. (Fig 3).

This change will mean that all products and services in the market, energy products and others, will have to be paid for with currency but also with a greater or lesser amount of energy permits, depending on the fossil fuel intensity of their production process.

Companies will have an incentive to charge to the consumers the amount of permits they need for their own energy consumption, because this is a way to get the permits for free, instead of buying them from the secondary market, in which they will have to pay for them This way, permits will travel through the value chain from the consumer to the energy suppliers. Energy suppliers will hand over the permits to the Public Agency that manages the system at the end of the period, just as in the traditional TEQs system.

Fig. 3 Circulation of P emission permits in the economy in EcoCore

The operating mechanism of Ecocore is described at this link: https://ecocore.org/proposal/

How do these decarbonization mechanisms make us co-responsible for reducing emissions?

These mechanisms would change the consumer and business behaviour in the following way :

In “Cap and Dividend” Citizens will have to pay a price increase for energy, not only in the energy invoices, but also in all goods and services, since the companies will also need to pay for the increase in energy prices, but on the other hand, citizens will also receive an amount of money as compensation for this extra cost. This subsidy will be paid for with the extra income received by the government from the sale of permits to energy companies. This extra income will be equally distributed among citizens allowing for people to pay for the higher cost of energy, goods and services, but the price increase will be lower in low-carbon energy, goods, and services, creating a competitive advantage for these options.

In “Tradable Energy Quotas” With this system (in both versions, ( TEQs or EcoCore), citizens don’t need to see their disposable income reduced to pay the carbon component of energy, since they are given permits to do that for free. Although the amount of permits received will be reduced year by year, citizens will have time to adapt accordingly with their decisions (purchase decisions, voting decisions, in the local and the global sphere).

Depending of the version of the TEQs system, the effects of each of these systems vary:

TEQs: Although citizens don’t have to see their disposable income reduced to pay for the carbon component of energy (petrol, electricity, etc.), they will have to pay for the carbon component of other goods and services. Since non-energy companies will have to buy the permits, they will tend to increase the prices of goods and services to compensate for that cost. In this regard, this system relies on the same mechanism as the Cap & Dividend system: citizens will have to pay a higher price for the fossil fuel component of goods and services due to the cost of the permits that companies need to pay. However, the price increase will be lower in low-carbon energy, goods, and services, creating a competitive advantage for these options.

Energy companies will need to adapt to a lower production each year, so they will need to downsize and/or switch to renewable energy sources. They will need to charge permits to their customers (individuals or companies) to hand them over to the Public Agency eventually, according to the quantities of each fuel sold and its particular carbon component.

The rest of companies: They will have to buy permits to pay for their energy invoices, so they will need to reduce their margin or raise their prices accordingly, at the same time that they will look for low-carbon alternatives to their inputs.

Import companies (non-energy companies), as any other company, will need to buy permits to pay for the carbon component of the foreign products or services they buy. This carbon component will have to be assessed according to some certification that assesses the carbon component of the products’ value chain.

EcoCore: in this version of the TEQs system, citizens don’t need to see their disposable income reduced to pay the carbon component of energy, like in the TEQS, but in this case they won’t have to pay for other goods and services’ carbon component either, since they will be given permits for free to pay for the carbon component of goods and services too.

Contrary to what happened in the «Cap & Dividend» or «TEQs» models, from the beginning, citizens will be able to see the carbon component of goods and services differentiated from price, so they will understand what consumption options are just cheap for other reasons and what are really low-carbon, and what consumption options are expensive for other reasons (quality, etc,) or a high-carbon component. This information will create a powerful signalling system to allow for a quick transformation of the productive system and the consumption patterns.

The rest of companies: This system will allow for companies to be transparent and charge permits to their customers for their goods and services to meet their permits’ needs for inputs (energy, goods, services…), and adapt their operations overtime to reduce their need for permits (i.e. their need for fossil fuels or fossil fuel intensive products or services). If they don’t want to be transparent and they don’t want to charge permits to their customers, they will have to buy the permits in the secondary market paying the market price for them, and reduce their margin or increase their products’ prices to compensate for the extra cost.

Import companies will need to buy permits upfront to pay for the carbon component of the foreign products or services they buy. This carbon component will have to be assessed according to some certification, unless the country of origin of such products has the same system, in which case permits could travel from country to country. Once the product is in the country, these companies will be able to compensate for the purchase of permits by charging them to their customers (individuals or distributors), so unless import quantities or carbon components change, they don’t need to get more permits.

Export companies: unless the country of destination of exports has the same system, they will need to buy permits to pay for their inputs in the initial sale of permits or in the secondary market, since they will be unable to charge their foreign customers for permits, so they will have to increase their prices accordingly. Nevertheless, these companies will be in a very good position to compete in markets that implement carbon controls, carbon taxes. ESG requirements, etc.

In conclusion

Much could be said about the details, the pros and cons of each of these proposals. We could discuss the obstacles to their implementation in Europe. We could discuss other tax-based modalities with similar objectives (Carbon fee and Dividend or others), but what we want to emphasize above all is the need to urgently implement effective measures to drastically reduce CO2, which can be acceptable to citizens and at the same time be consistent with the global carbon budget.

Although the vast majority of the world’s governments have signed the Paris agreements, they always find important or urgent reasons (fear of crises, riots, inflation, recession, wars, fuel shortages…) to postpone effective measures to comply. The latest IPCC report alerts us again that current national mitigation and adaptation pledges are not sufficient to keep us below 1.5°C or to reach the agreed adaptation targets. Putting a cap, a concrete limit on emissions in accordance with the carbon budget is the most transparent, most coherent and most understandable way for all citizens to realize how little margin we have left to avoid the risk of collapse. The equitable distribution of CO2 emission permits or of the profits from selling them, without the possibility of subterfuge or exceptions for some, is the best and quickest way for society to accept these limitations, assume its individual responsibility and collective changes to ensure our common future.